The Hybrid Buffer: Why Automakers Are Rebuilding for a Fragile Energy Decade

Why Hybrids, Ethanol Blending, and Battery Innovation May Shape the Next Phase of Mobility

△ ▼ △

Dispatches | By Beyond Coordinates

Over the last few weeks, I’ve been watching two stories move side by side: rising global EV adoption and renewed volatility around energy supply routes like the Strait of Hormuz. What caught my attention is how many automakers seem to be responding the same way: by building multiple paths at once through hybrid vehicles, cleaner combustion, solid-state battery programs, and long-term hydrogen bets.

Reader’s Note

As mobility enters a more complex transition, this dispatch looks at why automakers are investing across multiple technologies at once and what that could mean over the next few years.

For readers working across:

• Automotive & OEM leadership

• Energy transition & mobility infrastructure

• Manufacturing & industrial strategy

• Climate, policy & sustainability ecosystems

• Investors tracking transportation and battery innovation

• Operators observing EV, hybrid and fuel market shifts

Cross-post from the archives

This piece connects closely with “The Atoms of Power Fueling the Human Race” where I explored how energy systems shape industrial momentum far beyond fuel alone.

That earlier dispatch looked at power as civilizational infrastructure.

This week feels like a practical continuation of that idea.

This time, through the lens of mobility.

1. A transition moving with uncertainty

Over the last few weeks, I’ve found myself watching two stories unfold at the same time.

One sits in global energy markets. The other inside automotive boardrooms.

A meaningful share of global crude still moves through the Strait of Hormuz.

Even temporary disruptions there ripple across freight, logistics, and fuel pricing.

At the same time, EV demand keeps accelerating.

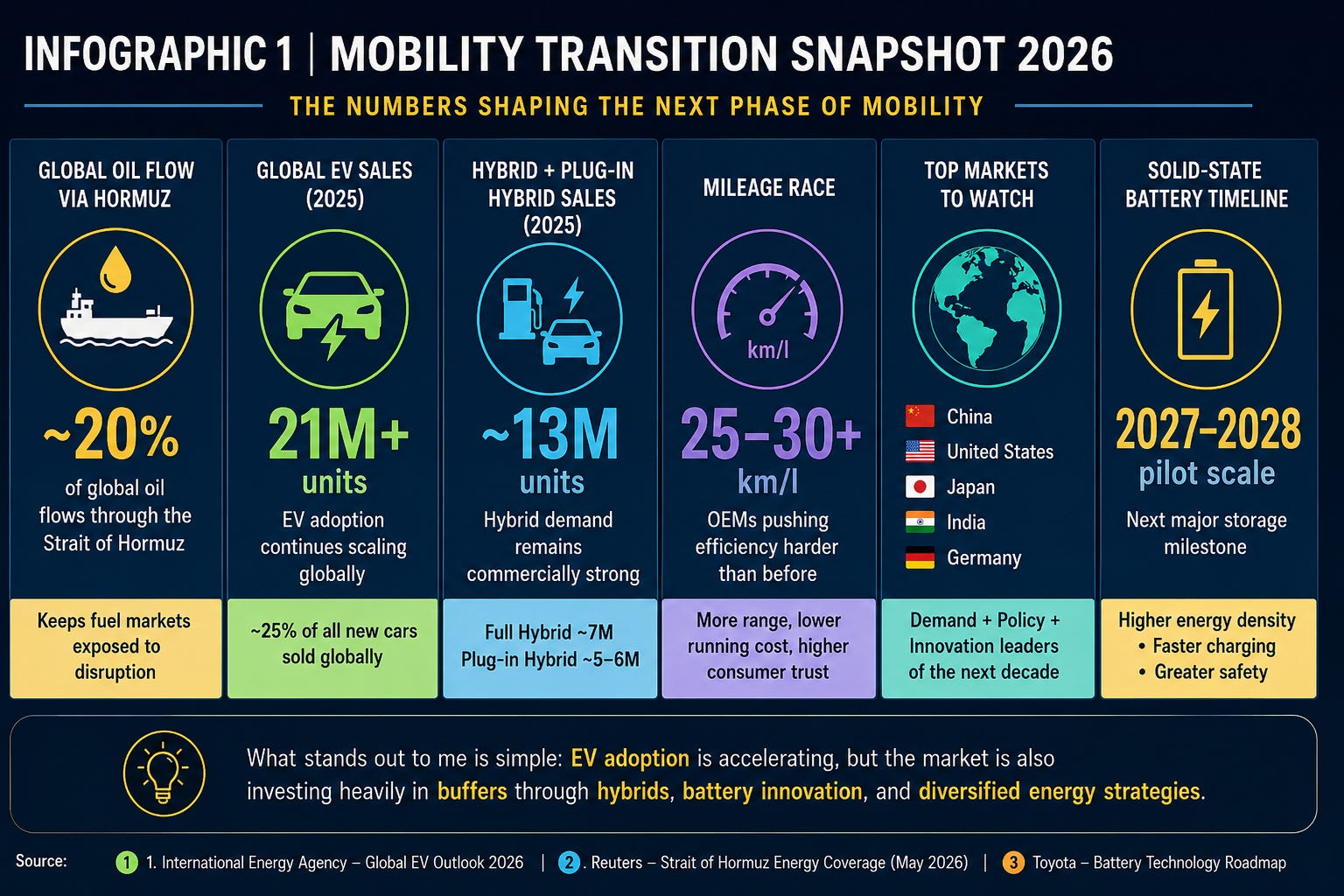

Global EV sales crossed 21 million vehicles in 2025, growing roughly 20% year over year and reaching nearly 25% of new car sales globally.

That is a major shift.

But what caught my attention is this:

The market is growing electric faster than before.

Yet automakers seem to be building more buffers than ever.

2. EV growth is real. Hybrid growth is too.

A lot of mobility headlines focus on EV momentum.

Fairly so.

But hybrids are quietly growing in parallel.

2025 snapshot

EVs

• 21 million units globally

Full hybrids

• 7 million+ units

Plug-in hybrids

• 5–6 million units

Mileage competition

• Many OEMs now targeting 25–30+ km/l in key segments

To me, this matters.

Because the market is not choosing only one lane.

Consumers still care about:

fuel costs

reliability

infrastructure access

affordability

And OEMs know it.

Transitions rarely move in straight lines. This snapshot captures the overlapping forces shaping mobility in 2026: rising EV adoption, hybrid resilience, battery innovation, and a global energy system still learning to absorb pressure.

2.5 Why hyper hybrids matter more in Asia

Another part of this transition feels easy to miss.

Fuel itself is changing.

In India, ethanol blending has already become a strategic national priority. The country has accelerated toward 20% and 27% blending, with broader flex-fuel discussions continuing around higher ethanol-compatible vehicles in the years ahead.

China is also expanding alternative fuel and energy diversification efforts as part of a wider push around energy security and reduced import dependence.

That changes how OEMs think.

Because the next generation of hybrids may not only balance battery and combustion.

They may also need to handle changing fuel blends more efficiently.

That is where hyper hybrids start to feel more relevant.

A stronger hybrid platform can help improve:

• battery-assisted efficiency in city traffic

• mileage over longer distances

• smoother adaptation to ethanol-blended petrol

• reduced dependence on imported crude

• better flexibility while charging infrastructure catches up

India’s ethanol push also carries practical trade-offs. Higher blending can strengthen fuel diversification and reduce crude dependence, but it also increases pressure on feedstock availability, water-intensive crop cycles, and import balancing in years when domestic supply falls short.

That makes the transition more layered than it first appears.

The ambition is clear.

The operating reality remains more complex.

There is also a practical side OEMs cannot ignore.

Higher ethanol blends may strengthen fuel resilience, but they also raise engineering questions around engine calibration, fuel-system durability, maintenance cycles, and long-term performance if vehicles are not optimized correctly.

That matters in Asia.

Large populations.

High fuel sensitivity.

Growing mobility demand.

And governments trying to improve energy security while keeping ownership affordable.

To me, that makes hyper hybrids feel less like a temporary category.

And more like a practical bridge built for markets balancing affordability, fuel diversification, and industrial transition all at once.

3. Five markets shaping the next phase

A few countries feel especially important right now.

China

Largest EV market globally.

Scale still unmatched.

United States

Strong EV demand.

Hybrid demand rising again.

Japan

Hybrid leadership remains strong.

Also one of the most important solid-state battery markets.

India

A practical mileage-driven market.

Huge long-term demand.

Germany

Regulation-heavy and strategically important for OEM transition.

These five feel like the mobility map to watch.

4. The OEM race is widening

What I’m noticing is not one race.

It feels like several.

Hybrid leaders

Toyota

Honda

Maruti Suzuki

EV-first challengers

BYD

Tesla

Solid-state battery innovators

QuantumScape

Samsung SDI

Toyota

Hydrogen & commercial transport

Hyundai Motor Company

Toyota

The more I look at this, the less it feels like one technology replacing another.

It feels like portfolio building under pressure.

The next chapter of mobility may not be shaped by one dominant technology alone. It may emerge through five major markets, multiple engineering paths, and a global industry learning how to adapt while demand and uncertainty rise together.

5. Why this transition feels different

What stands out to me most is how much more grounded the automotive conversation feels compared with a few years ago.

Back then, the debate often sounded absolute. EV versus combustion. Legacy versus future. One system replacing another.

This year feels more practical.

EV demand is still growing at scale. Hybrids continue gaining traction. Solid-state battery programs are moving closer to commercial timelines. Hydrogen remains selective but active. At the same time, oil supply routes remain exposed and infrastructure continues building unevenly across markets.

That combination matters.

Because automakers are no longer responding only to regulation or consumer preference. They are responding to geography, infrastructure, supply-chain pressure, and affordability all at once.

That changes the strategy.

The companies gaining momentum now appear less focused on proving one technology right and more focused on building multiple workable paths that can adapt as conditions shift.

To me, that feels less like hesitation and more like industrial realism.

6. Closing | The road ahead

The more I’ve watched mobility over the last few weeks, the more this transition feels layered.

Demand is growing quickly.

Energy markets remain sensitive.

Technology is improving.

And consumers still need practical choices they can trust.

That is why this moment feels important.

Sources & References

1. International Energy Agency — Global EV Outlook 2026

Global EV sales crossed 20 million in 2025, reaching roughly 25% of all new car sales worldwide, with continued momentum expected through 2026.

2. Reuters — Strait of Hormuz energy market coverage (May 2026)

Reuters’ recent coverage tracked oil shipping through the Strait of Hormuz and broader supply pressure, highlighting how roughly one-fifth of global oil supply remains exposed to disruptions in the region.

3. Toyota Europe — Battery Technology Roadmap

Toyota’s public roadmap outlines next-generation battery plans including solid-state battery commercialization targets around 2027–2028, with projected faster charging and improved range.

The road ahead may still become increasingly electric, but the transition itself looks broader than many expected. Hybrids are evolving faster, solid-state batteries are attracting serious attention, hydrogen remains relevant in commercial transport, and OEMs appear more willing to spread risk across several systems instead of forcing one answer too early.

That feels like the quiet story beneath the headlines.

A global industry learning how to move through uncertainty while demand keeps rising.

Not simply replacing one machine with another.

But building a stronger bridge between volatility and what comes next.

Some transitions arrive through disruption.

Others arrive by adapting faster than expected.

Copyright

© 2026 Beyond Coordinates All rights reserved.

This essay, including original analysis, narrative structure, infographics, and visual framing, is published as part of the Beyond Coordinates archive.

Independently verified for human authorship through GLTR and RADAR.