Carbon Credits and Regenerative Systems: The Carbon Ledger of a Changing Economy

How carbon markets, global policy, farm tech, and business demand are shaping a new income layer for agriculture

Reader note:

This Dispatch explores how regenerative agriculture is becoming part of financial infrastructure through carbon markets, AI-based measurement, and policy alignment. It looks at how soil carbon is verified and converted into income, and what this shift means for climate finance, ESG reporting, AgriTech, and enterprise decision making.

It is written for operators, investors, policy thinkers, and enterprise leaders navigating climate linked capital, ESG frameworks, and data driven reporting systems.

If you work in climate finance, agritech, ESG, or carbon markets, subscribe to follow this series.

▲▲▲

Dispatches | By Beyond Coordinates

I believe we’re entering a decade where farms stop being seen only as food-factories and start becoming climate-infrastructure. I think the “carbon ledger” of soil, water and biodiversity is already being written today — mostly in the background — and farmers are being asked to sign it, measure it, and monetise it. In this dispatch I more explore how regenerative agriculture earns credits, what recent climate summits signal, how top nations are moving, where technology is transforming fields, and what it means for business, consulting and everyday life.

Prologue: From Yield to Ledger

For most of my life, agriculture stories were about yield, cost, and maybe a new irrigation project.

Now I feel the vocabulary is changing. We hear about:

carbon sequestration

regenerative agriculture

soil-organic-carbon baselines

nature-based solutions

Behind these terms sits a simple question:

Can a farmer get paid not just for crops, but for healing the land?

I believe the answer is increasingly yes. But the “how” is complex, and sometimes over-technical. In this piece I want to keep the structure clear, human and practical — with full forms of key tech terms, some data points, and a few bullet sections where it helps.

Why the Carbon Ledger Matters Now

When I say “carbon ledger”, I’m thinking of a living balance sheet that records:

how much carbon a farm removes or stores (in soil, trees, biomass),

how much it emits (machines, fertiliser, processes),

how practices change this balance over time.

On top of that ledger, markets and policies are slowly building a new layer of value: carbon credits.

Carbon credit: a tradeable certificate for one tonne of carbon-dioxide equivalent (CO₂e) reduced or removed.

Voluntary Carbon Market (VCM): where companies and individuals voluntarily buy these credits to offset or compensate emissions.

I think this matters for three reasons:

Income diversification for farmers in a volatile climate and price environment.

Real climate impact, if measurement is honest and long-term.

Business strategy, as companies want credible, traceable low-carbon supply chains.

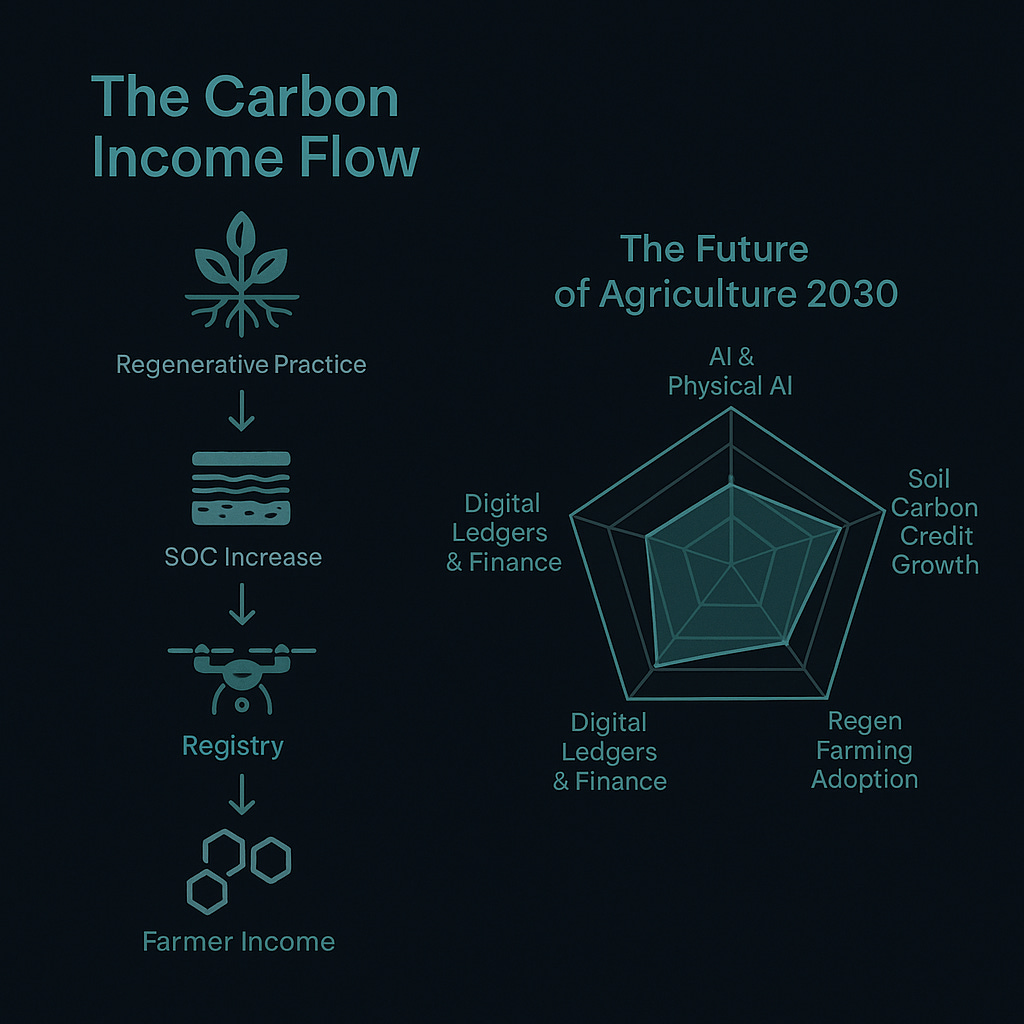

How a Regenerative Carbon Project Actually Works

I more feel many articles jump to big numbers without explaining the basic flow. Let me keep it simple.

Baseline

Measure current emissions and Soil Organic Carbon (SOC) levels.

Collect soil samples, satellite data, sometimes drone imagery.

Practice change

Move towards regenerative methods:

reduced or no-tillage,

cover crops,

crop rotation,

agroforestry (trees + crops),

organic inputs and better nutrient management.

Monitoring, Reporting and Verification (MRV)

MRV = Measurement, Reporting, Verification.

Sensors, farm logs, satellite data, and soil tests track how carbon levels change.

Independent verifiers validate the claims.

Issuance of carbon credits

Verified carbon gains become carbon credits in a registry or digital ledger.

Sale and revenue share

Credits are sold in voluntary markets.

Revenue is shared between farmers, project developers, tech providers, sometimes financiers.

I think of this like turning “good practice” into measurable, bankable value — a second income stream riding on the same land.

How regenerative practice becomes measurable, verifiable climate income — the full Carbon Ledger flow.

Tech Glossary: Terms, Full Forms & Field Reality

To avoid confusion, I more want to decode the jargon in one place.

AI – Artificial Intelligence

Models that process images, sensor readings and historical data to predict soil carbon, yield, and risk.UAV – Unmanned Aerial Vehicle

Drones used for:high-resolution farm mapping,

crop-health analysis,

detecting erosion,

verifying regenerative practices.

IoT – Internet of Things

Networked sensors placed in soil, pumps, weather stations and machinery sending continuous data on moisture, temperature, nutrients, usage.DLT – Distributed Ledger Technology (e.g., blockchain)

Shared databases that record carbon credits, ownership and transfers in a tamper-resistant way, reducing double-counting and fraud.SOC – Soil Organic Carbon

The carbon stored in soil organic matter. Higher SOC generally means healthier soil, better water retention and more resilience.MRV – Measurement, Reporting, Verification

The full process of collecting, documenting and independently confirming climate-impact data.

I feel once a reader has this glossary in mind, the rest of the conversation feels much less abstract.

Global Policy Signal: From COP Halls to Farm Gates

Every recent UN climate conference (COP) has carried a stronger undercurrent: we cannot hit climate targets without land-use and agriculture.

I see a few patterns:

More emphasis on Article 6 mechanisms under the Paris Agreement, which allow countries to trade emission reductions — including those from land and agriculture, if standards are robust.

Growing attention on “high-integrity” credits, with stricter rules around permanence, leakage and additionality.

Explicit mentions of regenerative agriculture, soil carbon and nature-based solutions in country pledges and roadmaps.

I believe this matters because it slowly de-risks the space. When global frameworks and national policies recognise regenerative projects, banks, insurers and large buyers feel more comfortable building long-term programs with farmers.

Nations on the Front Line (Top 5–7)

Without doing a country-by-country report, I more want to draw a quick map.

United States

Federal and state programmes supporting conservation and climate-smart practices.

Private carbon-programs paying farmers for regenerative adoption.

European Union

The Green Deal and Farm-to-Fork Strategy incentivising organic and regenerative approaches.

Movement towards common standards and “carbon farming” frameworks.

India

Large base of smallholders, rapid mobile and satellite penetration.

Pilots for carbon-farming, dairy and rice-methane reduction, and soil-health missions.

I think India’s mix of scale + digital public infrastructure makes it a potential outlier in adoption.

Brazil

Huge agricultural and forest landscapes.

Agroforestry, pasture restoration and rainforest-protection projects tied to carbon credits.

Australia

One of the earlier movers with soil-carbon and land-use credit schemes.

Grazing-land projects and rangeland regeneration integrated into national climate plans.

Canada & East Africa (Kenya, etc.)

Canada combining policy, incentives and data-driven projects across prairies and forests.

East African programs linking smallholder farmers to carbon finance, often via mobile platforms.

I believe these geographies are writing the playbook others will adapt in the next 5–10 years.

Business & Consulting Use Cases

Here I think bullet-points help, because the landscape is wide.

Core business models

Agritech platforms

Build end-to-end “carbon operating systems” for farms: onboarding, data capture, MRV, credit issuance and marketplace access.Carbon aggregators

Aggregate thousands of small farms into one large project, making credits export-scale and more attractive to big buyers.Banks and insurers

Use digital carbon ledgers to:offer better loan terms to regenerative farmers,

insure climate-smart practice,

underwrite multi-year projects.

Input companies and cooperatives

Shift towards regenerative-friendly inputs and build advisory programs around them, embedding carbon-farming in their business.Consulting firms

Design decarbonisation roadmaps for food and retail majors.

Create farm-to-fork supply-chain programmes tied to verified credits.

Build MRV and data-architecture for multinational portfolios.

The same mindset that values regenerative farms often shows up as thrift, repair and reuse in cities — different loops, but part of one larger circular story.

Tech on the Ground: Physical AI, UAVs and Carbon Sequencing

I think this is where the story becomes very “present day”.

When I say Physical AI, I mean AI systems that sense, decide and act in the physical world — not just on a screen. In agriculture this includes:

Drones (UAVs – Unmanned Aerial Vehicles) that autonomously survey fields, spray with precision, and detect stress hot-spots.

Semi-autonomous tractors and implements that optimise tillage depth, fuel use, and pattern of operations.

Smart irrigation systems that use AI on top of IoT sensor data to decide when and how much to water.

Carbon sequencing in practice:

Repeated soil sampling plus remote-sensing (satellite + UAV) over several years.

AI models that translate spectral signatures into SOC (Soil Organic Carbon) estimates.

Time-series “sequences” of SOC levels, showing how much carbon the soil is storing or losing.

I foresee MRV (Measurement, Reporting, Verification) costs dropping 70–80% as:

sensors get cheaper,

UAV coverage becomes routine,

AI models become more accurate with local data,

manual paperwork is replaced by digital workflows and ledgers.

The result is simple: more of every carbon-credit dollar can actually reach the farmer.

People & Homes: Signals from Technocrats and Balconies

There is also a quieter, human signal I can’t ignore.

I see more stories of people with strong résumés — graduates from institutes like IITs, IIMs, MIT, Harvard and similar — leaving high-paying corporate roles to start organic farms, natural-farming collectives, or regenerative agri-startups.

I believe this matters because:

it brings managerial, financial and technological skill back into the soil,

it gives farming a different kind of social and cultural status,

it creates live case-studies that investors and policymakers can point to.

At the same time, I notice residential dwellings, especially in tropical cities, quietly filling with:

balcony and terrace gardens,

small hydroponic / soilless units,

micro-greens and herbs grown at home,

I don’t want to over-romanticise this, but I feel these micro-farms change how people think about food, soil and effort. Over time, I foresee urban vertical gardens and community plots playing a small but symbolic role in broader regenerative ecosystems and maybe, one day, in micro-credit schemes linked to biodiversity or cooling benefits.

The Future (5–10 Years)

Based on every indicator I track, I foresee:

voluntary carbon markets hitting USD 20–40 billion,

soil carbon credits growing 16–26% CAGR (compound annual growth rate),

MRV costs dropping 70–80% through AI + UAVs,

regenerative adoption reaching 38–46% in major agricultural economies,

multi-asset credits (carbon + water + biodiversity) entering markets,

farms functioning as climate-infrastructure nodes,

Physical AI automating 30–40% of field operations,

digital carbon ledgers integrating directly with banks and insurers.

I more believe agriculture is about to become one of the most data-rich sectors globally. And yet, at the same time, I think its deepest value will still depend on very old things: trust, patience, seasons, and how we treat the ground beneath us.

Epilogue

When I look at this whole picture — COP halls, satellite dashboards, farmer fields, balconies, consulting decks — I feel we are sketching a new contract between civilization and soil.

The Carbon Ledger is not just an accounting tool. It is a quiet recognition that:

soil holds memory,

practices leave signatures,

and we finally have the tools to measure, reward and scale the good ones.

I think the next decade will decide whether this becomes a fair and farmer-centric system, or just another extractive layer on top of already-stressed lives. I trust that by naming both the opportunity and the risk, we can play our part a little more honestly.

For now, I see farmers slowly stepping into the role of climate stewards, sometimes without fanfare, sometimes without perfect data, but with a kind of practical courage that numbers alone can’t describe.

“When we learn to read the soil like a ledger, we also learn to remember that not everything of value fits into a line item.”

The Structural Shift

The carbon ledger is no longer a future concept. It reflects how biology is being measured, verified, and integrated into capital systems.

As carbon accounting matures, agriculture moves from yield optimization toward asset optimization. This shift influences ESG reporting, procurement strategy, climate disclosures, and long term enterprise risk.

Beyond Coordinates studies structural transitions across climate linked capital, AI infrastructure, and industrial transformation.

For collaboration or advisory conversations, you can reach out at jagrut.beyondcoordinates@gmail.com

Sources

FAO and World Bank briefs on soil carbon and regenerative agriculture, 2024 to 2025

Voluntary Carbon Market outlooks from BIS Research and Ecosystem Marketplace, 2024 to 2025

COP28 and COP29 high integrity carbon market frameworks

MRV, UAV and soil carbon AgriTech case studies, 2023 to 2025

© Beyond Coordinates 2026. Original research and analysis